When the board has finalized and agreed to the high level Vision, Mission, Goals and Objectives, management drafts a business (operational, facilities, staffing, etc.) plan (how will we achieve the strategic plan?) and an annual budget (how will we pay for it?) But your role is not yet complete, the final step of strategic planning is when the board approves the annual budget.

By reviewing and approving the budget, you have the opportunity to be confident that the Director of Education and staff have allocated sufficient resources, in the right places, to achieve the plan. Your review is not intended to be a detailed line-item by line-item check, rather the question you are asking is, “is this budget reasonable?”, “is it plausible that this proposed allocation of resources matches up with and can achieve the strategic plan?” This is a “macro” oversight not a “micro” management exercise.

Funding Components

You will want to be familiar with how School Boards are funded.

Expense categories are clearly delineated in School Board budgets and financial reports. These are:

- Governance: costs for boards executing your fiduciary responsibilities and duties, as well as elections, membership fees and dues, negotiating fees, public relations, SSBA research, policy and program decision making.

- Administration: education and business administration, including administrative salaries and non-salary items such as travel costs, computer supplies and software programs.

- Instruction: salaries and benefits of teachers, instructors, support staff, support specialists and school administration, broken down further into Base Instruction, School-Based Support, Supports for Learning, Locally Determined Terms and Conditions, and Instructional Resources: textbooks and library books, supplies and services including technology supports such as computer supplies and software programs, furniture and equipment, communications.

- Plant Operation and Maintenance: building operating costs for centralized instructional facilities and for maintaining school grounds, teacherages, storage facilities, maintenance workshops and warehouses.

- Complementary Services – Prekindergarten (PreK) component allocates funding to boards of education that operate ministry-designated PreK programs

- Transportation: including transportation operations and school bus renewal

- Tuition Fee Expense: to address fees typically charged for Saskatchewan students attending a school Outside the Provincial Public Education System

- Associate Schools: for the operation of associate schools with which you have a contractual agreement

- Debt Repayment: to provide for principal and interest payments associated with eligible ministry-approved borrowing

And there are two main sources of revenue for School Boards, each of which will be budgeted separately:

- Education Property Tax

- Grants-in-lieu of Taxes

You may also see (smaller) revenue items including tuition fee revenue, funding adjustments, transition and school consolidation assistance, other user fees and transfers, trust or investment income and fund-raising/donations/sponsorships/partnerships.

Your education operating funding grant is the calculated expense total minus the calculated revenue total.

The operating grant does not cover major building renovations or construction of new facilities. Boards of education receive a separate grant for building renovations and construction of new facilities.

You will want to be aware of the guiding principles that apply to how the Ministry will distribute funds to Boards of Education and how Boards of Education will allocate funds provided to them. The Ministry and Boards of Education will expect:

- Mutual Responsibility: be guided by sustainable programs and services that support the broad range of factors required for student achievement.

- Accountability: maintain a respectful collaborative working relationship, and ensure that the principles are reflected in their actions and decisions and demonstrate their responsibility to stakeholders and the public.

- Transparency: make decisions that are supported by evidence-based written policies that are consistently applied and easily understood.

- Equity: make decisions that support all students in reaching their full potential.

- Stability: make decisions that endeavour to provide the flexibility to deal with periods of economic stability, growth and decline.

Within this funding framework and consistent with these principles, School Boards have some flexibility in how they allocate resources to schools and initiatives, including local priorities.

For a complete review of funding components, you should access and read the Funding Manual here. http://www.education.gov.sk.ca/Ed-Finance/Distribution-of-Provincial-Funding

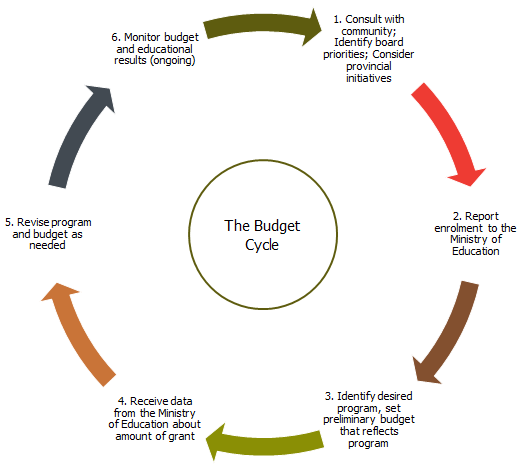

The Budget Cycle

The process used to develop the yearly budget varies from one School Board to another. It begins with identification of board priorities, and makes provision for ongoing monitoring to ensure the desired educational results are being achieved. Here is an overview of the budget cycle used by many School Boards:[1]

- Consult:

- Consult with the public and relevant groups: at the beginning of the budget cycle, the School Board may consult with the general public, School Division staff, parents, business groups and First Nations groups. This gives people (stakeholders) with differing opinions an opportunity to express their views about the programs and services they consider important. It also gives the board an opportunity to explain the financial implications of various packages of programs and services. For example, if the public asks for a huge expansion of technology-based programs, the board can explain that this might mean a reduction in other programs and services. This is an important component of a School board’s communications strategy.

- Identify Board Priorities: you may hold a formal strategy session each year (recommended) or you may set priorities through informal discussions. The board’s priorities are usually influenced by what the public says, changes in community needs or demographics, trends in education, and the board’s core values and beliefs.

The budget reflects the values and beliefs of the school system: the budget is one of the most powerful tools that a school board has for governing the school system. For example, school boards often identify core values and beliefs such as:

- Providing a safe, orderly, school environment

- Providing equality of opportunity and of outcomes for all students, and

- Preparing students for the technology-intensive, global economy of the future

During the budgeting process, you should ask yourself, “would this expenditure of money be consistent with our core beliefs and values?” and “with the outcomes we want to achieve?”

The board uses the budget and financial plan as a primary tool to achieve the strategic priorities of the School Division: you want to focus on results – on the type of student knowledge, skills and attitudes you want to see achieved. Although desired results often relate to retention rates and student achievement, many School Boards address other areas as well, such as students’ subjective experience of schooling, incidents of violence or bullying, and equality of outcomes for students of both genders and all cultural groups.

School boards also set long-term, short-term, and ongoing priorities. For example, building a new school is a long-term priority. Ensuring well-stocked, up-to-date school resource centres is an ongoing priority.

The way the School Board spends money should reflect the results the board wants to achieve and the priorities it sets, so you should:

- Write policies describing the results you want to achieve and the priorities you have established,

- Allocate resources to support your goals and priorities

- Monitor progress to ensure the desired results are being achieved

- Hold the Director of Education responsible for achieving the desired results

For example, if improving student retention is one of the board’s goals, then money would be allocated for supports that make it easier for students to stay in school. These supports might include anything from tutoring for students who are reading below grade level to daycare for teen moms.

- Consider Provincial Initiatives: Provincial priorities may include the implementation of new curricula, requirements concerning data collection and reporting, or programs to equalize opportunity for all students.

- Report Enrolment to the Ministry of Education: enrolment figures as of

September 30 must be reported to the Ministry of Education. The operating grant received from the Province is based largely on these numbers. - Identify Desired Program and Set Preliminary Budget: The School Board plans a package of programs and services and the Director of Education and Chief Financial Officer (CFO) develop a budget that reflects the board’s priorities. If you have a Finance Committee of your board, it will review the draft budget first and provide input to management and the board. During this process, some adjustments to programs, services and budget may be necessary in order to work within the anticipated revenue. Some questions for you to consider:

- What are the key risks to the plan?

- Assess the overall effectiveness and efficiency

- Perform Sensitivity Analysis (play “what if?”)

- Receive Budget Information from the Ministry of Education: The Ministry of Education uses September 30 enrolment figures to calculate the amount of provincial grant each School Division will receive. This information is provided to School Boards as soon as calculations are complete, usually late fall or early winter. Boards actually receive their provincial grant when the provincial budget comes down, usually in March of each year.

- Revise Program and Budget as Required: sometimes School Divisions have to adjust their preliminary program, budget and tentative mill rate once they know exactly how much money they will be getting from the Ministry of Education. You may decide to cut back on programs or you may be able to add program components. Final adjustments to the program and budget usually occur in March or April.

Monitor the Budget and Educational Results: to ensure money is being spent in accordance with priorities and that desired results are being achieved. Once you’re convinced that the annual budget provides the resources necessary to achieve the desired results, management implements the plan, and the cycle of measurement and adjustment begins.

[1] Adapted from Wagner and Sniderman, 1987